UPDATE | Prepare To Provide Paid Sick Leave and FMLA

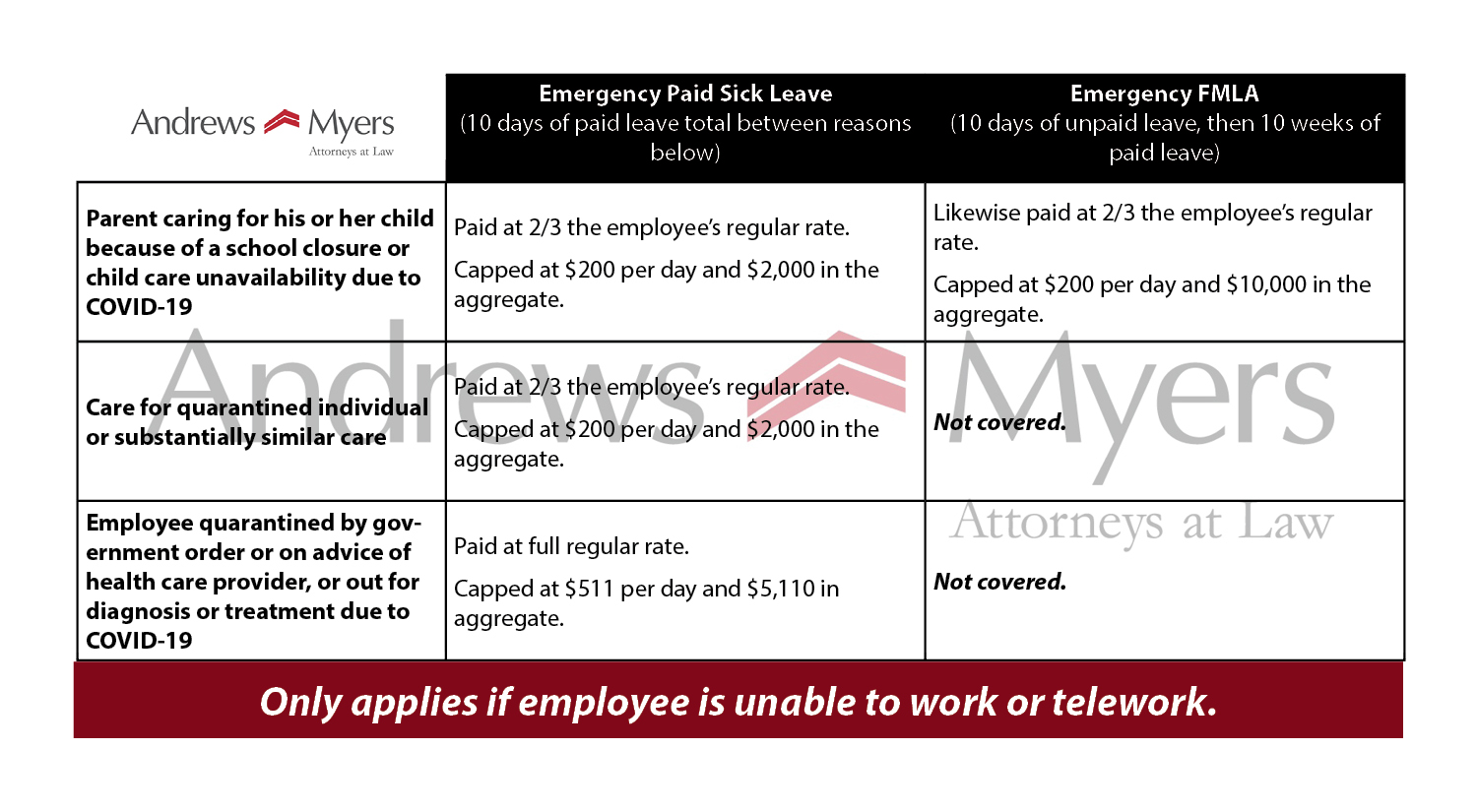

Houston — March 27, 2020 On March 18, 2020, President Trump signed the Families First Coronavirus Response Act (FFCRA), which requires businesses with under 500 employees to provide leave to employees missing work because of certain COVID-19 related reasons. You can find our previous article regarding employer’s FFCRA obligations here, as well as a chart briefly summarizing these obligations here.

Houston — March 27, 2020 On March 18, 2020, President Trump signed the Families First Coronavirus Response Act (FFCRA), which requires businesses with under 500 employees to provide leave to employees missing work because of certain COVID-19 related reasons. You can find our previous article regarding employer’s FFCRA obligations here, as well as a chart briefly summarizing these obligations here.

This week, the Department of Labor issued new guidance regarding these obligations, as well as guidance on related tax credits for employers who pay employees in accordance with the FFCRA.

Here are the updates employers need to know regarding their paid leave obligations:

- The FFCRA takes effect April 1, 2020—not April 2, 2020, the date most commentators believed would be the effective date. The FFCRA’s requirements are not retroactive. The FFCRA will still sunset on December 31, 2020.

- The DOL clarified that paid leave will be available employees who cannot work or telework and have a “bona fide need” for leave to care for an individual subject to quarantine or a child whose school or child care provider is closed or unavailable.

- There will be a small business exemption for employers will less than 50 employees for child care-related leave where the requirements would jeopardize the ability of the business to continue. Businesses claiming the exemption should document why they meet it, though they will not need to send materials to the DOL claiming the exemption. The DOL will release further guidance to more clearly articulate the exemption standard.

- The DOL confirmed that its joint employer and integrated employer tests will be utilized in determining whether the 500-employee threshold is met under the FFCRA.

- The model notice that has to be issued is available here and must be posted in a conspicuous location on employers’ premises. An employer may satisfy this requirement by emailing or direct mailing this notice to current employees, or posting this notice on an employee information internal or external website.

- For 30 days, the Department of Labor will not bring an enforcement action against any employer for violations of the FFCRA so long as the employer has acted reasonably and in good faith to comply with it. “Good faith” would exist if violations were not willful and are remedied.

The DOL, IRS, and the Department of Treasury announced a plan for how the FFCRA tax credit will work. This new release can be found here.

- Every dollar of required paid leave (plus the cost of a employer’s health insurance premiums during leave) will be 100%covered by a dollar-for-dollar refundable tax credit available to employers covered by the FFCRA.

- Qualifying wages are those paid to an employee who takes leave under the Act for a qualifying reason, up to the appropriate per diem and aggregate payment caps described in the chart provided above. Amounts paid over and above the FFCRA’s requirements will not be eligible for tax credits.

- In order to take immediate advantage of these credits, businesses can retain and access funds that they would otherwise pay to the IRS in payroll taxes. The payroll taxes that are available for retention include (1) withheld federal income taxes; (2) the employee share of Social Security and Medicare taxes; and (3) the employer share of Social Security and Medicare taxes with respect to all employees. Further guidance regarding this retention will be released next week.

- If an eligible employer does not have sufficient payroll taxes to cover the costs of qualified sick and child care paid leave, the employer can file a request for accelerated payment from the IRS. The IRS expects to process these requests in two weeks or less.

For more information please contact Tony Stergio or contributors Andy Clark and Elaine Howard.

###

Celebrating 30 Years in 2020

Founded in 1990, with offices in Houston and Austin, Andrews Myers, Attorneys at Law, is a corporate law firm and recognized market leader in Texas construction law. The firm focuses on the concentrated disciplines of commercial litigation, construction, commercial real estate, corporate and business transactions, with additional emphasis on related issues including bankruptcy and insolvency, energy, employment and capital formation. A seasoned team of attorneys provides timely and cost-effective solutions to the most complex problems facing entrepreneurs and middle-market industry leaders throughout the state and the nation. For more information please visit www.andrewsmyers.com.

{kind=link}

{kind=link}